I Moved to Texas to Make My Budget Work

The 6-layer framework I built for WealthOps after standard budgeting stopped working — and the move from California to Texas that made it real

👋 Managing Tech Millions by WealthOps 📈 your go-to source for building wealth with tech equity and managing the money that comes with it.

Every Thursday, we'll deliver a concise and powerful lesson on building wealth working for equity compensation or on managing your seven and eight-figure portfolio.

Today, in 5 minutes or less, you’ll learn:

📊 Why tactical budgeting (cut lattes, kill subscriptions) breaks once you have a real Foundation, real kids, and real complexity

🎯 The 6 layers of the Personal Capital Stack — and the three categories every layer falls into (structural, shock absorber, chosen investment)

🗺️ The single architectural move I made — California to Texas — that re-shaped my entire stack and freed up dollars for the things I actually wanted to invest in

Hey Portfolio CEOs,

A few years ago, I was sitting at the kitchen table in our Bay Area home, staring at a budget tracker, getting more stressed by the minute.

The mortgage was bigger than any rent we’d ever paid. We’d just had kids and the spending was going up everywhere I looked. My instinct was the one most people learn: cut the small stuff. Eliminate the lattes. Trim the subscriptions. Squeeze the discretionary line until the math closed.

It didn’t work. I was getting more stressed, not less.

Then I read Scott Trench’s Set for Life, and one line reframed how I think about money to this day:

Don’t try to save more on lattes. Take a swing at the big things — your taxes, your mortgage, your rent. That’s where you actually move the needle.

That insight saved me. But I needed something more than the insight — I needed a structured way to apply it inside the wealth I was trying to build. So I took Scott’s foundational reframe and built it out into a six-layer architectural model. I called it the Personal Capital Stack. Today it’s the lens we use inside WealthOps to look at every dollar that flows through a Family Office CEO’s life.

This newsletter is how it works.

Managing Tech Millions is a Weekly Podcast that gives you deep dive conversations into building and growing wealth with myself and other industry experts.

This week, I’m breaking down the operating system the wealthiest families in the world use to run their money — and how to build a scaled-down version even if you have $1M to $30M.

You’ve been asking the wrong question: Every book and advisor obsesses over where to invest. The real question once you’ve made the money is what’s the infrastructure around it. The wealthiest families don’t run a portfolio — they run a business. It’s called a family office, and it has 7 components.

Vision comes before everything: Component 1 is the one everyone skips — which is why the rest feels disorganized. Your Legacy Statement is the North Star. Your Investment Thesis is the filter every opportunity has to pass. Build these and FOMO disappears.

The Two-Company Architecture unlocks the tax savings: One entity protects your assets (The Vault). The other runs operations (The Engine). That separation enables the Deduction Stack — I paid my Certified Tax Planner $10K and saved $25K in year one.

You can’t run a business you can’t see: If you can’t answer your real net worth, after-tax returns, and tax projection in seconds, you don’t have an investment problem — you have a data problem.

Stop being the client. Start being the CEO: Traditional advisors tell you what to do. In a MiFO, you assemble a fractional team — and they execute within your strategy. Different relationship entirely.

Three Categories, Six Layers

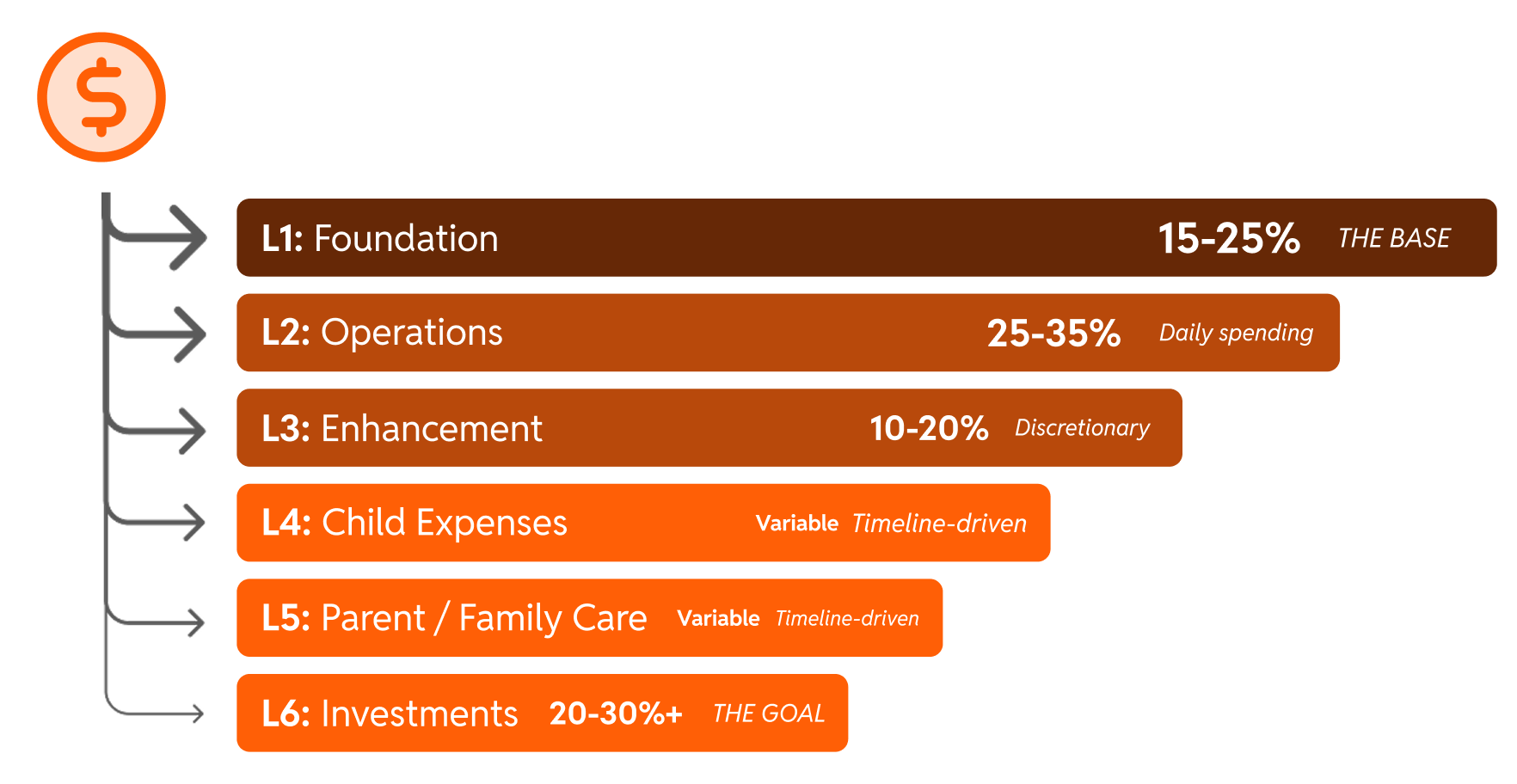

The Personal Capital Stack isn’t really six categories of spending. It’s six layers organized into three roles:

1. The Structural Layer (L1: Foundation) — The architected, fixed pieces of your life. Mortgage or rent. Property tax. Core insurance. Utilities. You don’t optimize this layer monthly. You make a structural choice about what your Foundation should be — and then you live around it. Target: 15-25% of income.

2. The Shock-Absorber Layers (L2: Operations + L3: Enhancement) — This is where life flexes.

L2 Operations (25-35%) is daily spending — groceries, gas, household, transportation, the subscriptions you actually use.

L3 Enhancement (10-20%) is discretionary — travel, dining out, hobbies.

Together, these layers are your shock absorber. When a lean season hits, this is where you cut. Fewer vacations. Cheaper gym. Less takeout. The whole point of having a clear shock absorber is so you know exactly where to flex when you need to — without panicking and slashing the wrong layer.

3. The Chosen Investment Layers (L4 + L5 + L6) — These are all forms of investment. The framework treats them differently than mainstream personal finance does — because they ARE investments, even when the dollars don’t go into a brokerage account.

L4 Child Expenses is your legacy investment. School. Activities. College. The next generation. You’re not “spending” on your kids — you’re investing in your legacy. The size flexes by season.

L5 Parent / Family Care is your family investment. Eldercare. Sibling support. Family obligations. Same logic — investment in the people that matter, scaled by season.

L6 Investments (20-30%+) is your dollar-per-dollar portfolio investment. What grows your wealth.

The whole stack exists to answer one question: what’s the maximum I can get into L4, L5, and L6 — without crushing the life I’m building?

The CEO Rule

Once you see the stack, the operating principle becomes obvious:

Manage every layer to maximize what reaches L6. Fat season — push hard. Lean season — protect what you can. The direction never changes. The volume does.

That’s the rule. Every dollar in L1-L3 is a dollar that didn’t make it to your investment layers. So the question stops being “how do I cut?” and becomes: “how do I architect each layer so the maximum amount of capital reaches investment — without breaking the life I’m trying to build?”

In a fat season — bonus comes in, equity vests, business has a great year — you push harder into L4, L5, L6. In a lean season, you protect what you can. The shock-absorber layers (L2 + L3) take the hit so the investment layers don’t. The Foundation stays where it is. The investment direction never changes — only the volume changes.

Don’t Eat Off Your Portfolio

The most important principle inside the stack — the rule the whole framework exists to enforce — is this: don’t eat off your portfolio.

We may go through months where we’re not adding new dollars to the portfolio. That’s fine. Lean seasons happen. But here’s what we will NEVER do: sell something inside the portfolio to fund our lifestyle.

The portfolio generates income. That income gets reinvested. The growth gets protected. If we have to flex, we flex the shock-absorber layers — not the engine.

That’s the difference between wealth that compounds and wealth that erodes. People who eat off their portfolio in lean years end up smaller every year. People who flex L2 and L3 instead end up larger every year — because the engine never stops compounding.

The Move That Made It Real

Once I had the stack mapped, I could see the structural problem clearly.

The Bay Area Foundation was too heavy. The mortgage was eating too much of our income, state income tax was eating more, and there wasn’t enough left over to fund the L4, L5, L6 layers the way we wanted to. I was nickel-and-diming the shock-absorber layers month after month, and it still wasn’t enough.

The move that fixed it wasn’t a budget move. It was a structural one.

We moved from California to Texas.

Lower mortgage. No state income tax. Suddenly the entire shape of our stack changed. The Foundation got smaller. The dollars we’d been chasing through tactical cuts started showing up automatically — at the architectural level.

What did we do with those freed-up dollars? We invested them where they mattered most: our kids’ education. Private school. The opportunity to raise them trilingual — French, Spanish, and English. And more into L6.

That’s what an architectural move looks like. You don’t optimize harder. You re-architect the structure so the dollars flow where you want them to.

How We Use This Inside WealthOps

This isn’t theory. The Personal Capital Stack is operationally embedded in how we run WealthOps.

The chart of accounts we use inside QuickBooks is structured by these layers. Every transaction gets categorized into L1 through L6. That means when we look at the data month over month and quarter over quarter, we can see exactly where the dollars went — and exactly which layer is over- or under-performing against our targets.

The data tells us what to adjust. The CEO makes the call. The architecture stays intact.

What This Framework Actually Enabled

I want to be specific about what this framework made possible — because the payoff is the whole point.

The Personal Capital Stack is what completed the build-out of my Micro Family Office. Once each layer was architected, the data was visible, and the operating rhythm was set, I had something I’d never had before: clarity about whether the machine was working. And it was working.

That’s what allowed me to walk away from the workforce in August 2022 and start living a life by design.

But here’s the part I want you to hear, because it’s the most important part of this entire newsletter:

The framework doesn’t tell you what to do. It tells you what to see.

These were the right decisions for us. The CA→TX move. The kids in private school. Trilingual. The percentages we set for each layer. The investments we made.

The right decisions for you will be different. And that’s the entire point.

Your Foundation. Your shock absorber. Your legacy investment. Your portfolio. The framework gives every layer a clear job. You decide what success looks like in each one. You decide the targets. You read the data. You make the calls.

This is about empowering you to use your own data to make the best decisions for the lifestyle you want — not copy mine. The whole point of this work is clarity and intentionality. The framework gives you the clarity. You bring the intention.

That’s the difference between living by default and living by design.

Key Takeaways

Tactical budgeting breaks at higher wealth levels. Cutting lattes can’t fix a too-heavy Foundation or a missing investment line. You have to architect, not optimize.

Six layers, three roles: Structural (L1) / Shock Absorber (L2-L3) / Chosen Investment (L4-L6). When you flex, you flex the shock absorber. You never raid the investment layers to fund lifestyle.

The framework empowers your decisions — it doesn’t dictate them. Your stack should reflect the life you want to build. Use the structure to gain clarity. Bring your own intentionality to the choices inside it.

Your Action This Week

Pull up your last three months of spending. Group every dollar into the six layers — Foundation, Operations, Enhancement, Child Expenses, Parent/Family Care, Investments.

Then ask yourself two questions:

First (the data): What percentage of every dollar I earned actually reached L4, L5, and L6 last month?

Second (the intention): Given the life I’m trying to build, is each layer doing the job I want it to do — or am I running someone else’s stack by default?

If you can’t answer either one, you don’t have a budgeting problem. You have an architecture problem. And that’s the one worth solving.

Let’s keep building.

—Christopher

P.S. The book that triggered all of this for me was Scott Trench’s Set for Life. Credit where it’s due — that book is worth your weekend if you’ve been stuck in the latte-cutting loop. The Personal Capital Stack is what came out of applying his core insight inside a Micro Family Office context, but the original reframe was his. You can find Scott on LinkedIn here.

Go Deeper

The role model underneath this: I Saw How the Ultra-Wealthy Actually Delegate — the Three Roles framework that determines what you own vs. what gets delegated.

Live workshop: The WealthOps Way — free, 2 hours. See how the Personal Capital Stack fits inside the larger Family Office operating system.

This is education, not advice. Learn the systems, don’t copy blindly.

Join me for The Micro Family Office Blueprint—our free live workshop designed to help you stop guessing and start running your wealth like a business.

You’ll go from scattered to strategic as you craft your own Portfolio Thesis—the foundation of everything that follows.

Spots are limited—and the clarity you’ll gain? Game-changing.

Let’s build your portfolio like it’s your next great company!

If you like the newsletter, support us by letting us know what you think (one click); please do that now!

PS...If you're enjoying Managing Tech Millions, please consider referring this edition to a friend.

And whenever you are ready, there three ways I can help you:

Follow me on LinkedIn: Get more insights and real-time updates.

Watch on YouTube: Dive deeper into wealth strategies and interviews.

Get in Touch: Ready for a bigger move? Let’s talk.

Disclaimer: This newsletter is for informational purposes only and does not constitute financial or career advice. Always consult with qualified professionals before making any decisions based on the information provided.