I Discovered How the Ultra-Wealthy Actually Build Portfolios

The metric that actually tells you if your portfolio is working — and it's not what you think

👋 Managing Tech Millions by WealthOps 📈 your go-to source for building wealth with tech equity and managing the money that comes with it.

Every Thursday, we'll deliver a concise and powerful lesson on building wealth working for equity compensation or on managing your seven and eight-figure portfolio.

Today, in 5 minutes or less, you’ll learn:

Why the drawdown model and the “money working for you” model are completely different architectures — and which one the ultra-wealthy actually use

The three-layer portfolio framework that reconciles the contradiction — and gives every dollar a specific job

A single question that replaces “what’s my number?” and reframes how you read your own portfolio

Hey Portfolio CEOs,

At some point, everyone asks the same question: “What’s my number?”

It’s the first thing you Google. The first thing you ask a financial advisor. The first thing that pops into your head when you start thinking seriously about your future. What’s the magic number where I can stop working?

And the plan behind that number is always the same: accumulate enough, then draw it down. Save $5M, withdraw 4% a year, and hope it lasts 30 years.

I remember the moment that stopped making sense to me. I sat with it and thought: Wait — the plan is to spend my entire career building this pile of money... so I can slowly watch it shrink to zero? That’s the goal? Get wealthy, then get progressively less wealthy for the rest of my life?

It didn’t add up. Especially when I’d read Rich Dad Poor Dad and Kiyosaki talks about getting to the investor quadrant — where your money works for you. Where assets generate income. Where you stop trading time for dollars. Money working for me and sending me checks — that’s supposed to be the destination. Not building up a big savings account and drawing it down.

So which is it? One model says accumulate and deplete. The other says build assets that pay you. These are two completely different philosophies — and nobody was reconciling them for me.

What is the truth? Why are they saying two different things?

That question plagued me for years. And when I finally got the answer, it changed how I think about every dollar in my portfolio.

Managing Tech Millions is a Weekly Podcast that gives you deep dive conversations into building and growing wealth with myself and other industry experts.

This week, I’m mapping every income asset available to investors with $1M–$30M portfolios—and showing you how to build a real income architecture instead of chasing yield.

The Income Ladder Framework: Why income assets aren’t one category—they’re three tiers with a specific sequence that matters

15 Income Vehicles Ranked: From T-bills and munis to syndications, BDCs, and private credit—what each one is and where it fits

The Yield Trap to Avoid: How to tell the difference between real yield and vehicles quietly returning your own capital back to you

5 Dimensions of Diversification: Why spreading across source type, liquidity, operator, tax treatment, and rate sensitivity is the real risk management

4 Questions Before Any Investment: The filter I use to evaluate every income asset before it enters my portfolio

The Breadcrumbs That Never Connected

For years, I kept picking up pieces of the second model. Rich Dad Poor Dad talked about assets that send you checks. I’d hear about ultra-wealthy families and their “income strategies.” I’d see data about family offices allocating 50%+ to alternatives that generate cash flow.

But none of it connected into a framework. None of it had a name. And the standard advice — from every advisor, every article, every retirement calculator — kept pushing the first model: accumulate, deplete, repeat.

I knew what Kiyosaki was describing. I just didn’t know how to build it.

You’re Not Picking Investments. You’re Blending Behaviors.

When my friend — who’d spent his career as CIO of family offices — finally laid it out for me, I realized they weren’t just picking better investments. They were working from a completely different blueprint.

Most retail financial advisors focus on one thing: Growth. Grow a big pile, then slowly deplete it in retirement. That’s the drawdown model — and now you know it’s not a legacy strategy.

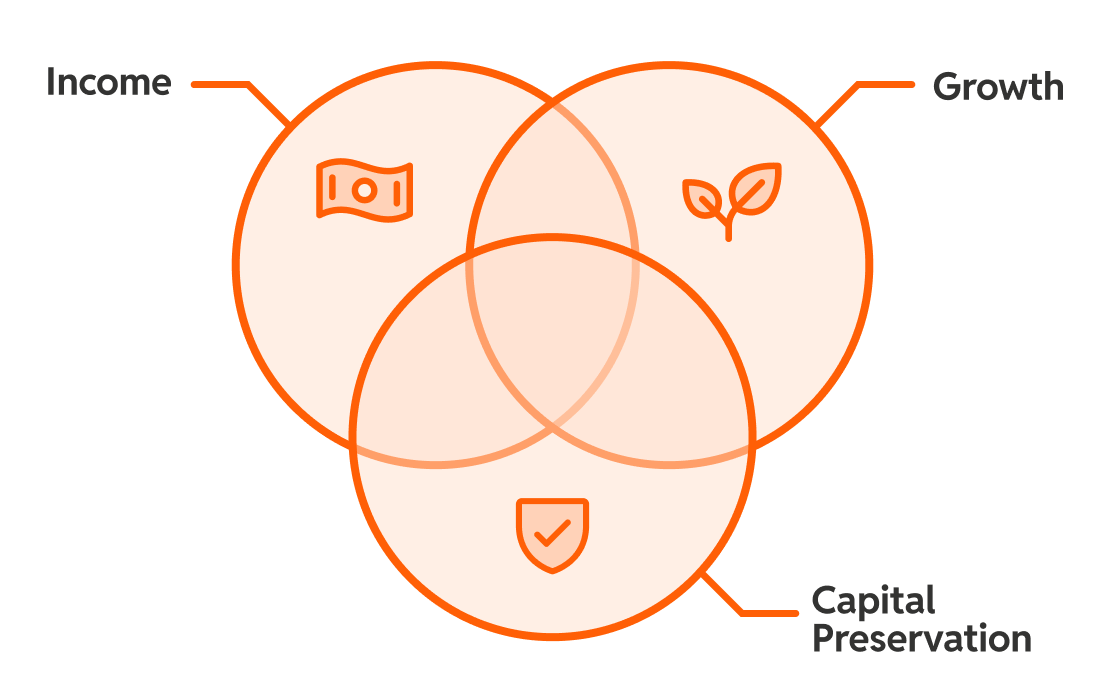

Family offices think about it completely differently. They don’t start with what to buy. They start with what the portfolio needs to do — and then they blend three behaviors together:

Income: How much does the portfolio need to generate to cover lifestyle? Not from selling assets. From distributions. Cash flow the portfolio produces while the principal stays intact.

Capital Preservation: How much needs to be protected to survive two years if income dried up or markets turned? That’s the backstop — what lets you ride out bad years without touching anything else.

Growth: What compounds over decades for the next generation? This only works because the other two behaviors are already handling lifestyle and risk.

Here’s the key: these aren’t three separate buckets. Think of them as a Venn diagram. The three behaviors overlap. You’re configuring a machine that does three things simultaneously — pays you today, protects your principal, and expands for the next generation.

That’s legacy-driven architecture.

You stop asking “How long will my money last?” and start asking “How do I configure this engine to run forever?”

The mix changes depending on your goals. Someone who needs to replace their paycheck next year blends differently than someone building a 30-year legacy. But the architecture is the same — three behaviors, customized to your situation, working together as one system.

The Light Bulb

When I heard this, it was like a riddle where the answer is obvious once someone says it out loud.

All those breadcrumbs — Rich Dad Poor Dad, the income investments, the family office data — they were all describing behaviors inside this same architecture. Kiyosaki’s “money working for you”? That’s the blended behavior — income, preservation, and growth working together. The financial advisor’s “grow a big pile”? That’s only the growth behavior, with no architecture around it.

They weren’t saying two different things. They were describing two completely different models. One is architected to create an outcome aligned with your goals. The other is designed for ease of management — a standardized offering advisors can scale across thousands of clients.

The drawdown model uses one behavior — growth — and then depletes it. You’re a storage vault. Fill it up, drain it down.

Legacy-driven architecture blends all three behaviors into an engine. Income funds your life. Preservation protects the system. Growth compounds because you never have to sell it. The principal stays. The engine runs.

Same starting capital. Opposite designs. Opposite outcomes over 20 years.

When I sat down and started configuring my own blend — plugging in my numbers, adjusting the mix for my goals — something clicked. Before, I’d been moving toward income but without a framework. After? I could see exactly how to configure the machine. How to model it. How to scale it as my wealth grew.

“I had all the pieces. They just didn’t have a name — and I didn’t know they were part of the same architecture.”

The Metric That Actually Matters

Here’s what this means for how you read your own portfolio:

Net worth tells you how much capital you’re sitting on. That’s useful. But it doesn’t tell you if that capital is doing anything.

Income capability tells you what your portfolio can generate. That’s the metric the ultra-wealthy actually track.

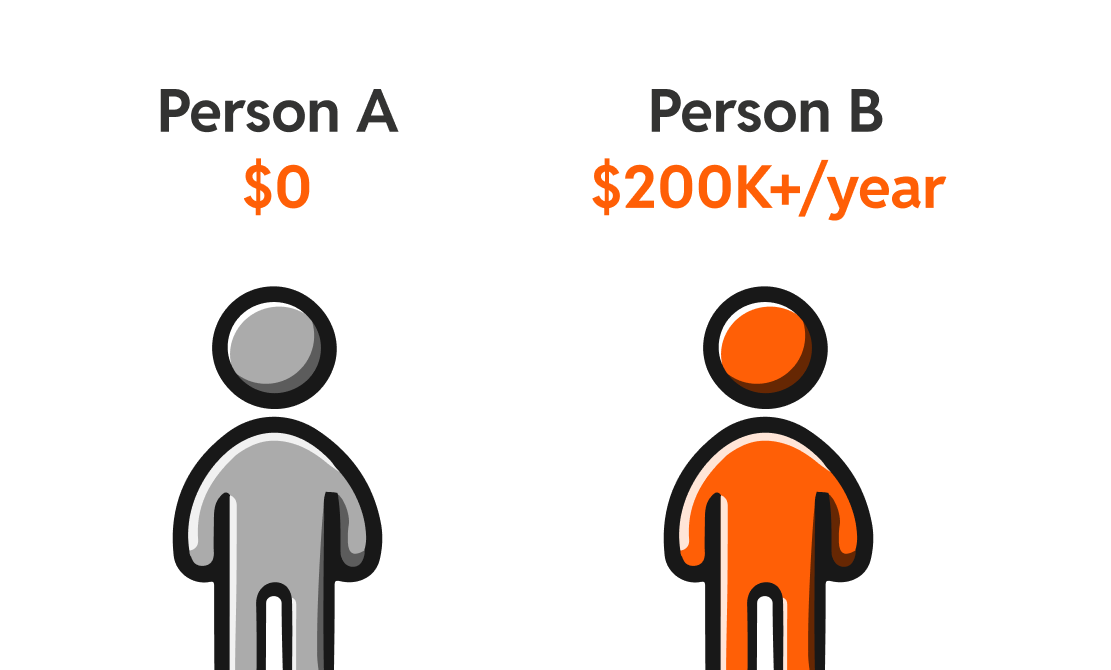

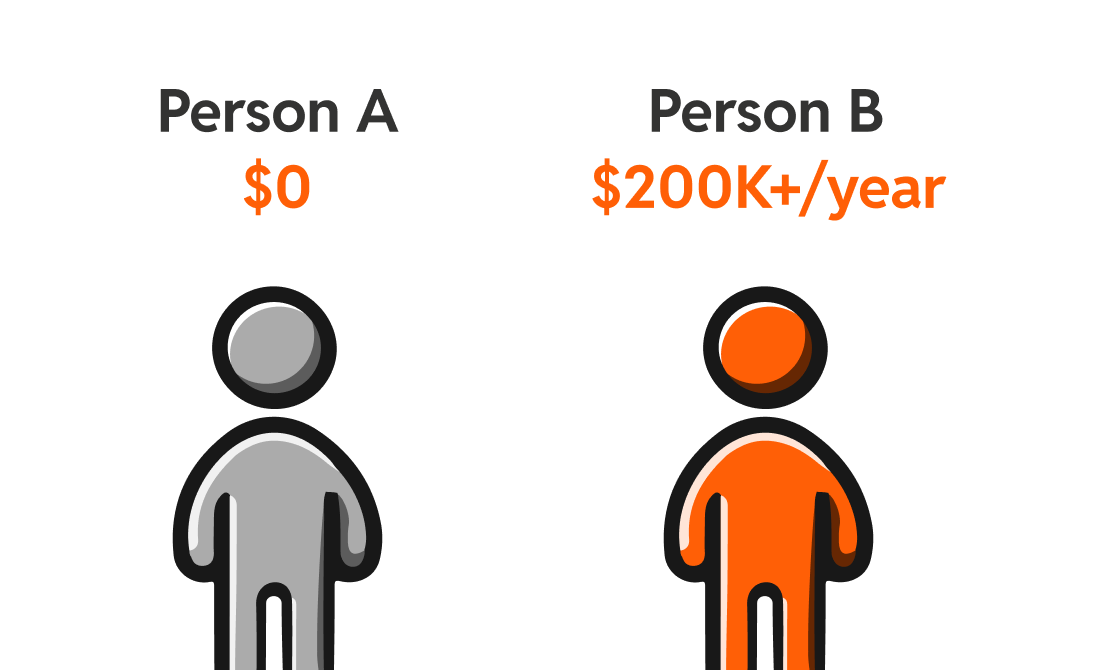

Two people with $5M portfolios can be in completely different positions:

Person A: $5M in index funds and growth stocks. Portfolio income: $0. Remove the W-2 and they start selling assets to live.

Person B: $5M structured across income, preservation, and growth layers. Portfolio income: $200K+/year. Remove the W-2 and nothing changes.

Same net worth. Opposite realities. The difference isn’t how much they have — it’s how their capital is architected.

That’s UHNW Principle 2: Generate income from assets, not asset sales.

The question isn’t “what’s my number?” The question is: “Can my portfolio cover my lifestyle without selling anything?”

Key Takeaways

The drawdown model and the “money working for you” model aren’t two opinions — they’re two completely different architectures. The ultra-wealthy use the second one.

Family offices architect top-down: Income first (cover lifestyle), Capital Preservation second (survive downturns), Growth third (compound over time). The order matters. The layers reinforce each other.

Income capability is the metric that matters — not net worth. How much your portfolio generates without selling assets tells you if you’re actually making progress.

Your Action This Week

Stop asking “what’s my number?” and start asking a better question:

How much did my portfolio pay me last month?

Not what it grew by. Not what it’s worth on paper. What it actually deposited into your account — distributions, dividends, cash flow.

Write that number down. That’s your income capability today. That’s where you’re starting from. And now you know the architecture that gets you from here to “W-2 optional.”

Let’s keep building.

—Christopher

P.S. Next week: the meeting that made me rethink everything I thought I knew about advisors — and the questions I should have been asking from the start.

Join me for The Micro Family Office Blueprint—our free live workshop designed to help you stop guessing and start running your wealth like a business.

You’ll go from scattered to strategic as you craft your own Portfolio Thesis—the foundation of everything that follows.

Spots are limited—and the clarity you’ll gain? Game-changing.

Let’s build your portfolio like it’s your next great company!

If you like the newsletter, support us by letting us know what you think (one click); please do that now!

PS...If you're enjoying Managing Tech Millions, please consider referring this edition to a friend.

And whenever you are ready, there three ways I can help you:

Follow me on LinkedIn: Get more insights and real-time updates.

Watch on YouTube: Dive deeper into wealth strategies and interviews.

Get in Touch: Ready for a bigger move? Let’s talk.

Disclaimer: This newsletter is for informational purposes only and does not constitute financial or career advice. Always consult with qualified professionals before making any decisions based on the information provided.