The Lie About Portfolio Income That Keeps You Working Forever

Why selling assets isn't income—and the 3-category framework that creates real cash flow

👋 Managing Tech Millions 📈 your go-to source for building wealth with tech equity and managing the money that comes with it.

Every Thursday, we'll deliver a concise and powerful lesson on building wealth working for equity compensation or on managing your seven and eight-figure portfolio.

Today, in 5 minutes or less, you’ll learn:

🏦 The 3-category framework that turns your portfolio into a cash-flowing machine

💰 Why asset categories make all the difference in building generational wealth

📊 The shift from depletion to income-focused wealth management

Hey Portfolio CEOs,

Christopher here.

There’s a massive lie in traditional wealth management that’s keeping you chained to your desk.

The lie? “You’ll generate retirement income by selling 4% of your portfolio every year.” That’s not income. That’s slow-motion liquidation.

Real income means your assets pay you while keeping your principal intact. The difference isn’t semantic—it’s the difference between temporary wealth and generational wealth.

Today I’m showing you the exact three-category framework that transformed my portfolio from a concentrated stock position into a cash-flowing machine—without depleting a single dollar of principal.

Managing Tech Millions is a Weekly Podcast that gives you deep dive conversations into building and growing wealth with myself and other industry experts.

This week, I’m showing you how the ultra-wealthy allocate their portfolios—and how you can model their strategies for greater returns and less risk.

The 23% Rule: Why the ultra-wealthy put only 23% in public stocks—and why you should too

Beyond the Stock Market: How real estate and private equity generate passive income and hedge against inflation

Strategic Financial Planning: Why having a diversified portfolio is essential for long-term wealth

Protect Against Volatility: How non-public assets provide stability and tax advantages

Wealth-Building Machine: How to implement these strategies and transform your portfolio

The 4% Depletion Myth They Teach

Here’s what every traditional advisor preaches:

“Save up a big portfolio, then sell 4% annually to fund your lifestyle.”

Let’s call this what it really is: eating your seed corn.

When you sell assets for “income”:

You trigger tax events every single time

Market crashes force you to sell at the worst possible moments

Your principal shrinks year after year

You’re literally betting you’ll die before the money runs out

This isn’t a retirement strategy. It’s a depletion countdown.

Meanwhile, there’s an entirely different approach that the ultra wealthy use—one where assets pay you to own them.

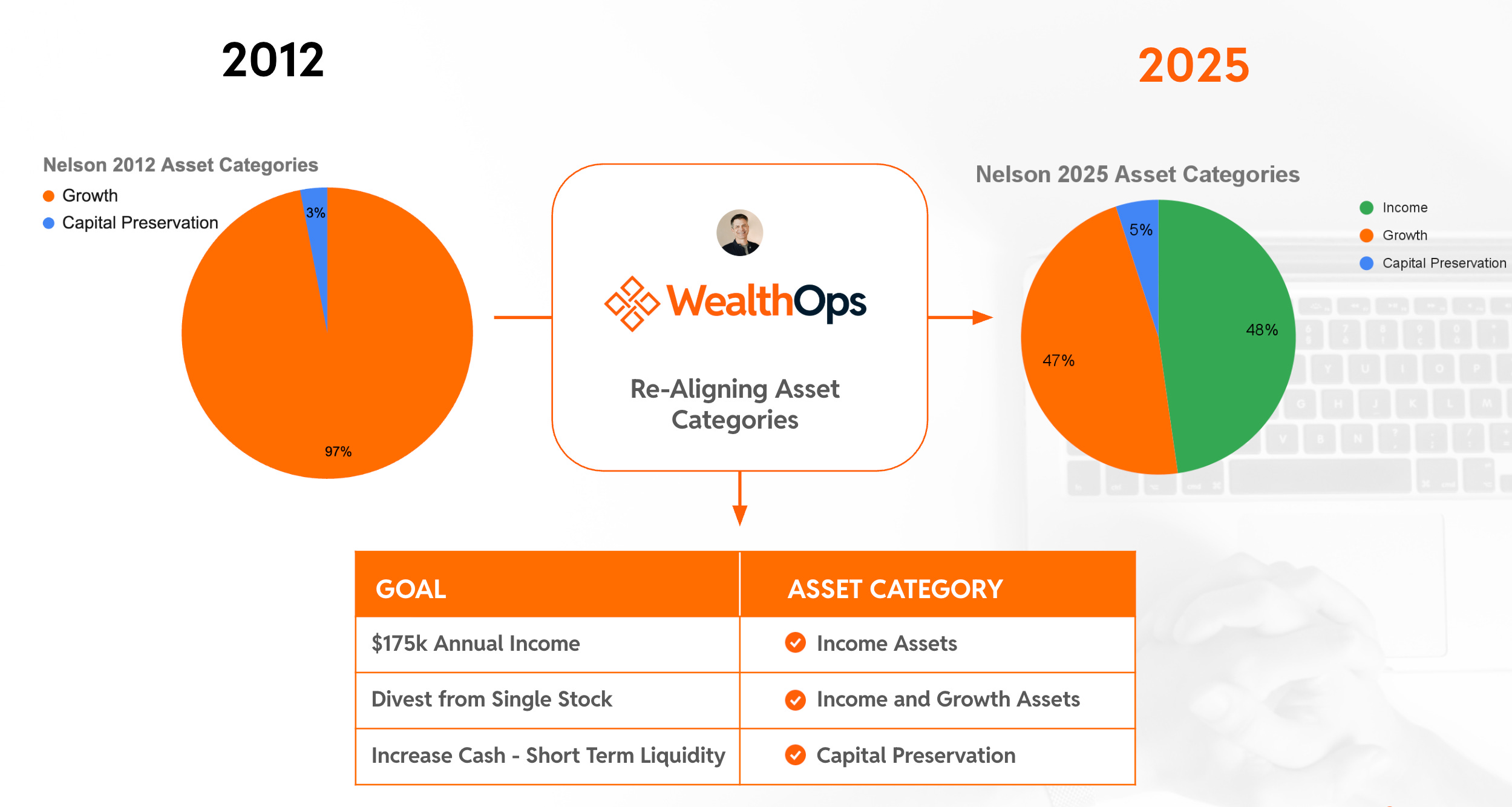

My Wake-Up Call: From Concentration to Categories

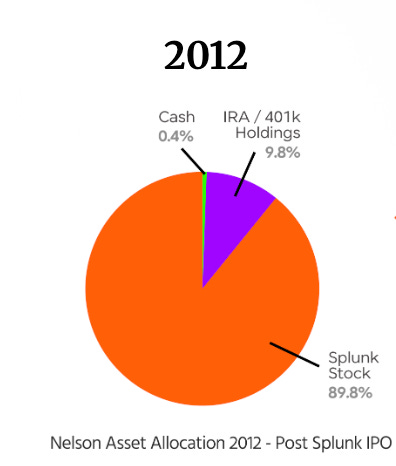

In 2012, after Splunk’s IPO, my portfolio looked like this:

89.8% in Splunk stock (hello, concentration risk)

10.2% in retirement accounts and cash

Income generated: Almost nothing

Everyone looked at this pie chart and said “you need to diversify!”

Sure, but diversify INTO WHAT?

That’s when I discovered the power of asset categories—not just spreading money around, but deliberately choosing assets based on what job I needed them to do.

The Three-Category Framework That Changes Everything

Here’s the breakthrough: Instead of random diversification, I aligned every investment with a specific goal using three categories:

Capital Preservation (5%)

Goal: Increase cash and short-term liquidity Purpose: Sleep-at-night money, opportunity fund Assets: T-bills, high-yield savings

Income Assets (48%)

Goal: Generate $175K annual income Purpose: Replace W-2 without selling principal Assets: Real estate, private credit, REITs, dividend stocks

Growth Assets (47%)

Goal: Divest from single stock, build long-term wealth Purpose: Future appreciation and legacy building Assets: Diversified equities, private equity, venture

The transformation wasn’t just about spreading risk—it was about engineering portfolio behavior.

I stopped asking “what should I buy” and started asking “what job does this asset need to do?”

Real Income vs. Fake Income: The Difference That Matters

Let me be crystal clear about what separates wealth preservation from wealth depletion:

FAKE INCOME (The 4% Rule)

Sell assets every year

Trigger capital gains taxes

Deplete principal over time

Pray markets cooperate

Work until you have “enough”

REAL INCOME (Asset Categories)

Assets pay distributions/dividends

Different (often better) tax treatment

Principal stays intact or grows

Income flows regardless of market prices

Work becomes optional faster

When your income comes from assets paying you—not from selling those assets—everything changes.

Why Most People Stay Stuck in Depletion Mode

Three reasons tech professionals never escape the 4% depletion trap:

1. They don’t know income assets exist beyond bonds Your advisor won’t mention private credit funds paying 8-10%. Or real estate syndications distributing 6-12%. Or business development companies yielding 7-9%. These don’t generate commissions for them.

2. They think in net worth, not cash flow Having $5M means nothing if it doesn’t generate income. But $2M in the right income assets? That’s $200K annually without touching principal.

3. They never categorize with intention Without clear categories, you’re just spreading money around hoping something works. With categories, every dollar has a specific job.

The Simple Framework You Can Implement

Stop thinking about individual investments. Start thinking about portfolio architecture:

Step 1: Define Your Three Categories

Preservation: How much do you need liquid for emergencies/opportunities?

Income: What annual cash flow replaces your salary?

Growth: What builds generational wealth?

Step 2: Map Your Current Holdings Take every investment you own. Assign it to ONE primary category based on its main job. You’ll immediately see the gaps.

Step 3: Set Target Allocations

Conservative: 20% Preservation / 50% Income / 30% Growth

Balanced: 10% Preservation / 45% Income / 45% Growth

Aggressive: 5% Preservation / 40% Income / 55% Growth

Step 4: Reallocate With Purpose Don’t dump everything at once. Systematically shift from your current state to target state, considering taxes and timing.

Your Portfolio Audit Starts Now

Here’s what I need you to do this week:

The 10-Minute Category Audit:

List every investment you own

Mark each as P (Preservation), I (Income), or G (Growth)

Calculate the percentage in each category

Answer this: What percentage of your portfolio generates cash without selling assets?

If your answer to #4 is less than 30%, you’re playing the depletion game whether you realize it or not.

The shift from depletion to income isn’t complicated. It just requires seeing your portfolio differently.

Instead of a pile of assets you’ll eventually sell, see it as a machine engineered to pay you forever.

The wealthy don’t sell assets to live. They own assets that pay them to live.

Which game are you playing?

Stay systematic,

Christopher Nelson Engineering income, not managing depletion

PS: Forward this to someone still believing the 4% rule is a retirement strategy. They need to know that selling isn’t income—it’s just organized liquidation.

Join me for The WealthOps Way—our free live masterclass designed to help you stop guessing and start running your wealth like a business.

You’ll go from scattered to strategic as you craft your own Portfolio Thesis—the foundation of everything that follows.

Clarify your long-term vision

Define your next best investment move

Build the system that turns wealth into freedom

Choose your class:

Spots are limited—and the clarity you’ll gain? Game-changing.

Let’s build your portfolio like it’s your next great company!

If you like the newsletter, support us by letting us know what you think (one click); please do that now!

PS...If you're enjoying Managing Tech Millions, please consider referring this edition to a friend.

And whenever you are ready, there three ways I can help you:

Follow me on LinkedIn: Get more insights and real-time updates.

Tune into the Podcast: Dive deeper into wealth strategies and interviews.

Get in Touch: Ready for a bigger move? Let’s talk.

Disclaimer: This newsletter is for informational purposes only and does not constitute financial or career advice. Always consult with qualified professionals before making any decisions based on the information provided.