Why I Built Two Companies for My Money

I didn't invent the Two-Company Architecture — I scaled down what family offices and investment businesses already do. And here's the part most people get wrong about why it matters.

👋 Managing Tech Millions by WealthOps 📈 your go-to source for building wealth with tech equity and managing the money that comes with it.

Every Thursday, we'll deliver a concise and powerful lesson on building wealth working for equity compensation or on managing your seven and eight-figure portfolio.

Today, in 5 minutes or less, you’ll learn:

📊 The shift that makes this matter: why portfolio income deserves a business structure even when your W-2 doesn’t

🎯 The 4 questions I ask before adding ANY complexity to my Family Office (entity, advisor, account, system)

🗺️ Why I landed on the Two-Company Architecture — and why the framework matters more than the specific answer

Hey Micro Family Office CEOs,

Most newsletters about entity structure want to make you feel like you’ve discovered a secret. I want to do the opposite.

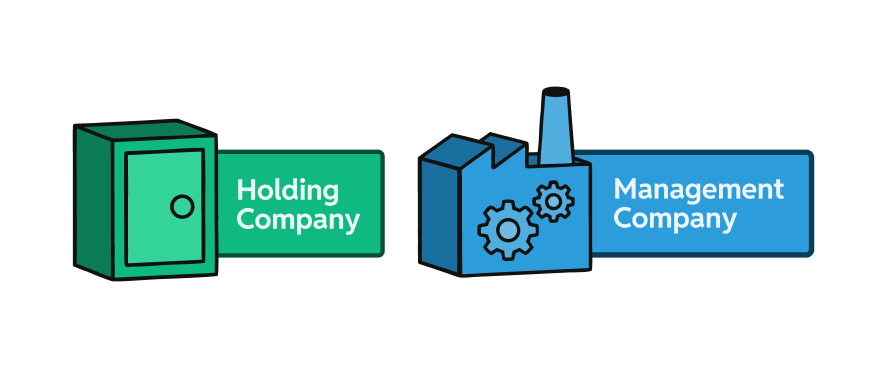

When I built the Two-Company Architecture inside my Micro Family Office — the Holding Company that owns and protects, plus the Management Company that operates and generates income — I didn’t invent any of it. I learned it. From studying family offices and other investment-type businesses. Then I scaled it down to fit my situation.

Before I go further, I have to set context — because this is the most-misread topic in personal finance.

This newsletter is NOT about reducing your W-2 / ordinary income tax. Your paycheck is your paycheck. There are smart things you can do at the margins, but the structure I’m about to walk you through doesn’t apply to your day job income. If that’s what you’re looking for, this isn’t it.

What this IS about: building a business around your portfolio income. When the goal is to replace your paycheck with portfolio distributions — when your wealth is generating real cash flow and you want to live off it — there’s a giant difference between (a) taking that income personally at ordinary individual rates and (b) running it through a properly structured business that family offices and investment shops have used for decades.

Without that structure, your portfolio income gets taxed at a much higher effective rate than it has to — because you’re not leveraging any of the tools available inside a properly-structured business. With the right structure, that same income flows through an entity designed for it — accessing deductions, business expense reimbursements, retirement contributions, and treatment that personal taxpayers simply don’t have access to. Same dollars from your portfolio. Materially different effective tax rate, depending on the wrapper around it.

I started studying family offices in 2014 because I wanted to know exactly that: I want to replace my ordinary income paycheck with my portfolio income — how do they actually do it, and can I scale it down?

That question, and the framework I used to answer it, is the most useful piece of thinking I’ve developed for evaluating any complexity decision in my Family Office.

Managing Tech Millions is a Weekly Podcast that gives you deep dive conversations into building and growing wealth with myself and other industry experts.

This week, I’m ranking every income investment available to you—and the ones pushed hardest on YouTube aren’t the ones I’d recommend.

The Evergreen Model: Build a portfolio that pays you without depleting principal—the framework most retirement plans miss entirely.

The Grading Criteria: I rank all 15 income vehicles S through F using yield, liquidity, and time to learn for a specific persona—$5M, five years out, growth-stock background.

The S-Tier Pick: The cleanest on-ramp from growth stocks to income isn’t a dividend ETF—and it’s not what most investors expect.

Why “Popular” Doesn’t Mean “Right Fit”: Real estate syndications and private credit get pitched everywhere—both score D for someone with a 5-year retirement horizon.

Five Dimensions of Diversification: Owning more vehicles isn’t the same as being diversified. Real diversification spans source, liquidity, operator, tax treatment, and rate sensitivity.

The Shift That Makes This Matter

Most people don’t think of their portfolio — or their personal finances — as a business. That’s a middle-class mindset.

When you start looking at how the ultra-wealthy operate, you see something different. They look at everything as a business. They measure. They manage. They’re consistent. And they surround everything with entities — because entities do two things that personal ownership never can:

1. Defense. Entities reduce liability and legal risk. Your assets are no longer in your personal name — they’re owned by a structure designed to protect them. There’s a phrase the ultra-wealthy live by that captures this perfectly: “Own nothing, control everything.”

2. Tax efficiency. Entities give you access to deductions, business expense reimbursements, retirement contributions, and treatment that personal taxpayers simply don’t have access to.

When I first started thinking about entities, defense was the priority. How do I get my hard-earned dollars out of my personal name and into a structure that protects them? The second question was: how do I build that structure so it’s also tax-efficient?

That’s when I started studying how family offices and investment businesses are structured. Not to find loopholes. To learn the playbook these structures have used for decades — and figure out how to bring it down to my level.

The Sequence I Actually Built (Stage by Stage)

I didn’t build the Two-Company Architecture all at once. I built it in stages, as the wealth and the income grew. The sequence matters — most people try to skip stages and end up with structure they’re not ready to operate.

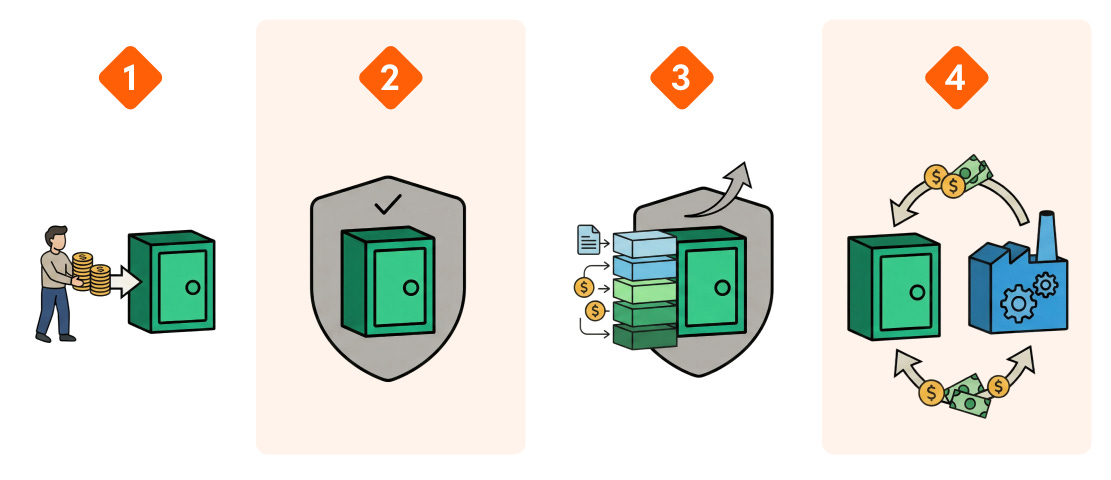

Stage 1: I started with a Holding Company. A single entity that let me take my hard-earned dollars out of my personal name and into a structure designed to hold and protect them. This was the defensive move first — getting assets out of personal exposure.

Stage 2: I made my Trust the owner of the Holding Company. This wrapped the entire entity in another layer of legal protection — and rolled the assets inside it into the same trust that drives my long-term estate plan. Two layers of structure, working together.

Stage 3: I started taking legitimate expenses against the Holding Company. This is where I really started understanding the concept of the “Deduction Stack” — the systematic series of legitimate, defensible deductions a properly-structured entity can take. The Deduction Stack has multiple levels (we teach the full stack inside the Accelerator), but the foundational layer started right here, inside this Holding Company. Suddenly the entity wasn’t just defensive — it was producing meaningful tax efficiency too.

Stage 4: I added the Management Company when the portfolio income justified it. When my portfolio started producing $30,000 to $35,000 a year in income, I’d hit the threshold where I was running a real business — generating real cash flow with real operations. That’s when adding the Management Company started to make sense. The Management Company became the operating entity — generating, managing, and taxing the portfolio income through a proper business structure designed for exactly that.

The sequence matters. Most people who try to set up a Two-Company Architecture jump straight to both entities before they have the income to justify the second one. That’s expensive, complicated, and creates compliance overhead before there’s any business activity to justify it. The right way is to start with the Holding Company for protection, build it correctly, take the foundational deductions, and add the Management Company when the income earns it.

The 4 Questions I Ask Before Adding Any Complexity

Here’s the part most people skip — and it’s the part that matters most.

Adding complexity to your financial life is dangerous if it isn’t earned. A second entity that you don’t operate properly is worse than no entity at all. A trust you don’t fund is paperwork that creates false confidence. A tax strategy you can’t defend is a future audit.

So before I add any complexity — entities, advisors, accounts, systems, anything — I run it through four questions:

1. What’s the maximum ROI for the minimum complexity?

Every layer of structure has an operational cost. Bookkeeping. Tax filings. Annual maintenance. The structure has to deserve that cost. If the upside doesn’t materially exceed the overhead, skip it.

2. Is it defensible?

If a competent tax attorney looked at this structure — or, more importantly, if the IRS asked questions — does it hold up cleanly? You’re not looking for “creative.” You’re looking for “obvious.” If you can’t explain why the structure exists in plain language, that’s a red flag.

3. How many people are using this?

Is this how every operating business in America is structured, or is this an avant-garde edge case? Mainstream is your friend. The further you drift from common business practice, the more risk and the less defensibility you have. I’m not interested in being clever. I’m interested in doing what actually works.

4. Can I actually run it?

Will I be able to stand this up and operate it inside my real life — with the bookkeeper, the CPA, the systems I have? Or is this a beautiful spreadsheet that will collapse in execution? An unfunded structure is a liability. A structure you can’t operate is theater.

If a complexity decision passes all four questions, it goes in. If any of them are weak, I either simplify it or wait.

Have You Thought About Whether This Could Be For You?

If any of this is sparking the question “could I do this?” — good. That’s exactly the question worth sitting with.

But before you act, run the decision through the same four questions any business owner asks before adding any complexity to their business. I didn’t decide on a Holding Company in a weekend. I did real due diligence. I reflected on each of these. The questions are the work.

1. What’s the ROI?

Start with the upside. For the Two-Company Architecture, the ROI is genuinely substantial — better effective tax rates on portfolio income inside the operating entity, plus separation of business operations from personal liability. The combination is one of the highest-leverage structural moves available. The math works at the right income level. If the upside isn’t real and meaningful, no other answer matters.

2. What’s the complexity?

Every layer of structure has a cost. Two entities mean two sets of books, two filings, two annual maintenance loads. Inter-entity transactions need to be documented. Each entity has its own setup expense, its own ongoing CPA work, its own legal hygiene. The complexity is real. The question is whether the ROI from #1 materially exceeds it. For Two-Company at the right income level, it does. Below that level, the complexity isn’t worth carrying yet.

3. What’s the risk?

This is where most people get into trouble. Risk has two dimensions: Is the structure defensible if challenged? and Is this mainstream business practice or are you out on a limb? For Two-Company Architecture, both answers are clean. Family offices, investment partnerships, and wealth management businesses use some version of this structure as a matter of course. It’s textbook architecture, just applied to portfolio income. There’s nothing creative — and that’s the point. Creative gets you audited. Mainstream gets you confidence.

4. Can you actually run it?

This is the question most people skip — and it’s where most people fail. Two entities require two sets of books. They require quarterly bookkeeping reviews, careful documentation of inter-entity transactions, formal annual filings, and a CPA who’s filed multi-entity returns before. An entity you don’t operate properly is worse than no entity at all. It creates compliance risk and false confidence at the same time. So the answer to “can I run it?” can never be aspirational. It has to be operationally honest. Do you have the bookkeeping infrastructure? Do you have the CPA? Will you actually maintain quarterly notes? If yes — proceed. If no — wait until you do.

These are the same questions every CEO asks before launching anything new in their business. ROI. Complexity. Risk. Operability. The Two-Company Architecture is just a wealth-side version of a business decision. There’s nothing exotic about the question set. The only question is whether you’ve actually sat down and answered all four — honestly — before you act.

For me, all four came back positive. So I built it.

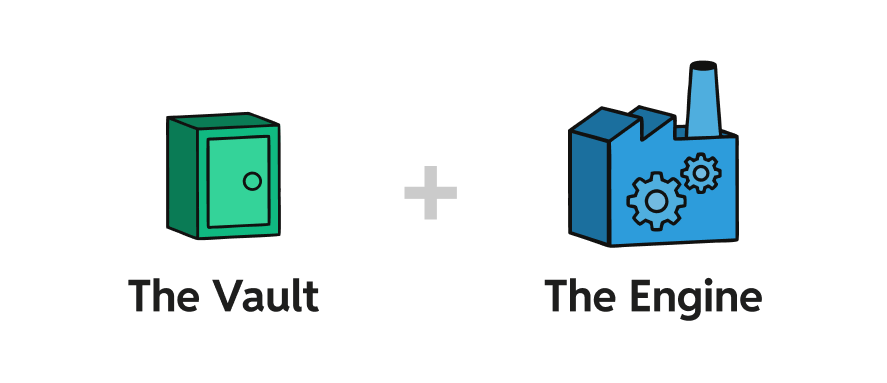

The Holding Company became my Vault — it owns and protects assets long-term. The Management Company became my Engine — it operates, generates income from the portfolio, and accesses the tax structure that real investment businesses use. Two companies, one architecture, doing different jobs together.

The Meta-Lesson Beneath the Architecture

Here’s what I want you to take from this — even more than the entity structure itself:

The breakthrough wasn’t the answer. It was the question.

I didn’t sit down and decide “I’ll have two companies.” I sat down and asked what do family offices and investment businesses do, and can I scale it down? The Two-Company Architecture was the answer that came out of that question. But for someone else — different stage, different wealth, different family situation — the answer might look different. The question is what’s universal.

Every Family Office CEO faces the same complexity decisions over and over. Should I form an entity? Should I hire a CPA? Should I open a separate account? Should I add a tax strategy? These questions never stop. The four-question filter (ROI / Complexity / Risk / Operability) is what keeps complexity from getting away from you — and what makes sure the complexity you DO take on is actually earning its keep.

Common business sense, applied at the right scale. That’s the whole game. I’m not interested in being avant-garde. I’m interested in being right.

And here’s the most important point — the reason this newsletter exists in the first place:

There are real, substantial benefits to operating wealth this way. They’re not theoretical. They’re not reserved for billionaires. They’re available to any Family Office CEO who’s reached the right stage and is willing to do the work. You just need to be educated. That’s it. The structures aren’t secret. The strategies aren’t hidden. The playbook isn’t gated behind a $25M minimum. What’s been gated is the education — the ability to see the architecture, evaluate it for yourself, and decide whether you’re ready to build it.

That’s what we’re doing here. Not selling you anything. Teaching you how the structures actually work, what questions to ask, and how to know when you’re ready. Education is the unlock.

Key Takeaways

Family offices and investment businesses operate portfolio income through entity structures by design — not by exception. Bringing that architecture down to your scale isn’t aggressive planning. It’s how proper investment businesses have been structured for decades. The Two-Company Architecture is one specific way to apply it.

Before adding any complexity, run it through four questions: ROI / Complexity / Risk / Operability. These are the same questions every CEO asks before launching anything new. Pass all four = go. Fail any = wait or simplify.

The benefits are real — and they’re not gated behind some impossible threshold. What’s been gated is the education. Understand the architecture, ask the right questions, and you can evaluate (and eventually build) what fits your situation. That’s the entire point of doing this work.

Your Action This Week

Pick the most recent piece of complexity you’ve added — or are considering — in your financial life. An LLC, an advisor relationship, a new account type, a tax strategy, anything.

Run it through the four questions every business owner asks:

What’s the ROI?

What’s the complexity?

What’s the risk?

Can I actually run it?

If you can’t answer all four cleanly, the structure isn’t earning its keep yet — and that’s worth knowing before it costs you.

Let’s keep building.

—Christopher

P.S. If this newsletter dropped you into the middle of a conversation that felt like it was missing context — that’s because it was. Two-Company Architecture is not where you start. It’s something you build toward once you have the Family Office foundation in place.

If you haven’t yet seen that foundation laid out — what a Micro Family Office actually is, the two portfolio models, the 7 Components, and how to write your own Legacy Statement — The WealthOps Way is where to start. It’s a free 2-hour live workshop where I walk you through the foundation. No pitch. Just the framework, taught from the beginning.

👉 Sign up for the next session here: wealthops.io/go

If you want to learn how a Family Office actually works — start here.

Go Deeper

🎯 Start here if you’re new to this — The WealthOps Way Free, 2-hour live workshop. The foundation: what a Micro Family Office is, the two portfolio models (Drawdown vs Evergreen), the 7 Components, and your own Legacy Statement. Best entry point if you want to learn how a Family Office actually works from the beginning.

The architectural reframe behind this: I Moved to Texas to Make My Budget Work — the architectural-vs-tactical thinking that informs every structural decision.

This is education, not advice. Tax laws change frequently — verify current rules with qualified professionals. Learn the systems, don’t copy blindly.

Join me for The Micro Family Office Blueprint—our free live workshop designed to help you stop guessing and start running your wealth like a business.

You’ll go from scattered to strategic as you craft your own Portfolio Thesis—the foundation of everything that follows.

Spots are limited—and the clarity you’ll gain? Game-changing.

Let’s build your portfolio like it’s your next great company!

If you like the newsletter, support us by letting us know what you think (one click); please do that now!

PS...If you're enjoying Managing Tech Millions, please consider referring this edition to a friend.

If this was useful, tap the ❤️ button. It tells Substack to show more writing like this.

And whenever you are ready, there three ways I can help you:

Follow me on LinkedIn: Get more insights and real-time updates.

Watch on YouTube: Dive deeper into wealth strategies and interviews.

Get in Touch: Ready for a bigger move? Let’s talk.

Disclaimer: This newsletter is for informational purposes only and does not constitute financial or career advice. Always consult with qualified professionals before making any decisions based on the information provided.