I Paid My CPA $10K. It Saved Me $22K.

The CPA conversation that saved me $14K in year one — and the credentials most people don’t know to look for

👋 Managing Tech Millions by WealthOps 📈 your go-to source for building wealth with tech equity and managing the money that comes with it.

Every Thursday, we'll deliver a concise and powerful lesson on building wealth working for equity compensation or on managing your seven and eight-figure portfolio.

Today, in 4 minutes or less, you’ll learn:

📊 The one question that reveals whether a professional service is actually expensive — or a bargain disguised as a fee

🎯 The exact conversation that changed how I evaluate every advisor, CPA, and specialist I work with

🗺️ Why “what does it cost?” is the question that keeps most people stuck — and what to ask instead

Hey Micro Family Office CEOs,

Last week I walked through the Two-Company Architecture — and the four questions every business owner asks before adding complexity. The hardest one was the last one: can you actually run it?

Two entities need two sets of books. A CPA who’s filed multi-entity returns. Quarterly bookkeeping reviews. Real operational hygiene. Without those people in place, the architecture collapses.

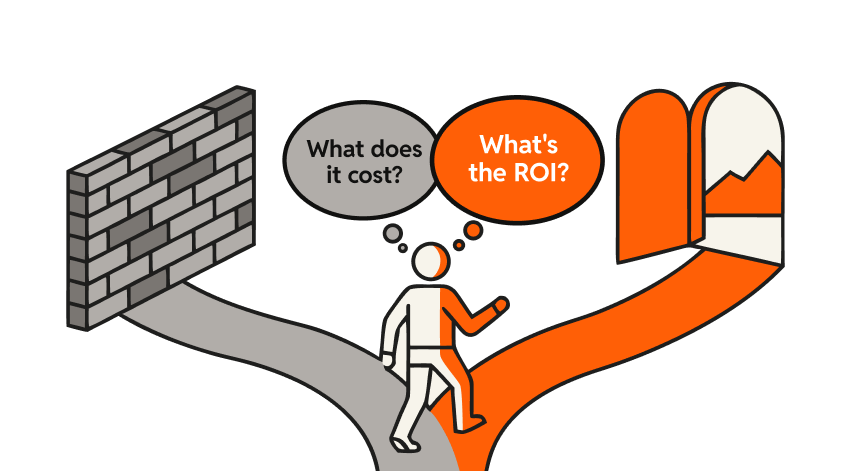

But here’s the question almost everyone asks the wrong way when it comes to hiring those people: “how much does it cost?”

I asked it that way for years too. And I left a lot of money on the table doing it.

Then I sat down with two Certified Tax Planners — John and Greg — and they reframed the entire conversation in about thirty seconds. What they told me has stuck with me ever since, and it’s now the lens I use to evaluate every professional I hire.

Managing Tech Millions is a Weekly Podcast that gives you deep dive conversations into building and growing wealth with myself and other industry experts.

This week, I’m walking through the 5 counter-intuitive principles that helped me retire at 51—and why the conventional retirement playbook wasn’t built for people trying to retire early, generate durable income, and leave a legacy.

Beat the IRS, Not the Market: A 2% improvement in after-tax returns compounds faster than chasing extra market performance—and unlike the market, you actually control it.

Build an Orchard, Not a Silo: Stop building a portfolio designed to be drained. Build one that produces income season after season without consuming principal.

Run Your Wealth Like a Business: A multi-million dollar portfolio with no operating cadence, no governance, and no plan isn't a strategy—it's a hobby.

Become the CEO, Not the Admin: Your advisor shouldn't sit at the center of your wealth org chart. You should. They're specialists in their lane—you own the strategy.

Build for Year 5, Not Year 1: Concentrated stock, alternative allocations, income streams—none of it transitions overnight. If you wait until you need the portfolio to perform differently, you're already behind.

The Conversation

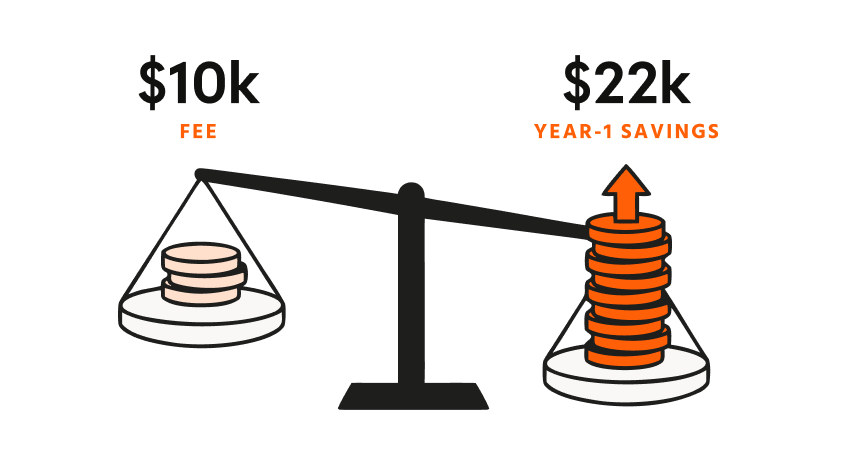

When I was vetting John and Greg, they quoted me their fee: $10,000.

If I’d evaluated that the way most people evaluate professional services, I would have done a quick gut check (”is $10K a lot for tax planning?”) and either flinched or shrugged. Either way, the framing would have been: this is a cost.

But they didn’t let the conversation stop there. They walked me through the actual tax plays they were going to implement in year one — the structures, the deductions, the timing. Then they showed me the number on the other side: $22,000 in projected first-year tax savings.

The math is suddenly different:

Cost: $10,000

Year-one savings: $22,000

Net ROI in year one: $14,000

That’s not an expense. That’s a 140% return on capital deployed — in twelve months — fully documented, fully defensible. And that’s just year one. The structures they put in place compound year after year.

The fee was real. But the fee was also the lowest-leverage thing in the conversation.

Wait — What Kind of CPA Is This?

That’s the question I want you to be asking right now. And it’s exactly the right one.

Most people pick a CPA and stop there. The reality is the CPA category is huge. It runs from people doing financial audits at corporations, to people doing personal tax preparation, to people running every other kind of accounting work in between. They all share the same three letters. The skills vary enormously.

What most people don’t know: within the CPAs who do your taxes, the very best ones are the proactive ones. And they signal that proactivity by earning additional credentials — like the Certified Tax Planner (CTP) designation, or Certified Tax Strategist (CTS).

A CTP or a CTS isn’t a different profession. They’re CPAs who’ve specialized in proactive tax strategy — designing plays before the year ends, not just reporting on what happened after it.

Here’s the shift those credentials signal:

A reactive CPA tells you what you owe.

A proactive CPA — a CTP or CTS — helps you plan to pay less.

That’s the whole game. The difference between “what you pay” and “what we planned, so you don’t have to pay it” is exactly where John and Greg added the $14K of value in year one. They’re CPAs. They’re also CTPs. The first set of letters got them in the door. The second set is why they could quote me a savings number, not just a fee.

If you have a CPA, that’s the floor. The next level: a CPA who’s also earned one of those proactive credentials — or who at minimum operates proactively and is willing to have an ROI conversation with you.

The Lens This Gives You

Once you’ve had the ROI conversation with a strategist, you can’t unsee it. Every professional service starts looking different.

Your CPA isn’t an expense — they’re either keeping you legal at an acceptable cost, or they’re not. Your bookkeeper isn’t overhead — they’re either freeing your time (measurable value) or they’re not. Your Certified Tax Planner isn’t a luxury — they’re a profit center, measured in dollars saved, not dollars charged.

This is how the ultra-wealthy think about every professional on their team. Not “what does it cost?” but “what’s the ROI?” A great strategist is happy to have that conversation with you. A weak one will dodge it.

That’s also how you tell the difference between the two.

The Reframe

Here’s the question I now ask before hiring anyone:

“Walk me through what I’d be paying you, and what I’d realistically expect to get back in the first year — in dollar terms.”

A few things happen when you ask this:

Strong professionals welcome it. They’ve done the math before. They can show you specific plays, specific savings, specific outcomes for clients like you. They want you to understand the value they bring. The ROI conversation is the conversation they prefer.

Weak professionals dodge it. They’ll talk about “experience,” “service quality,” “personal attention” — all real things, but none of them are dollar-denominated. If they can’t put a number on what you’ll get back, they probably haven’t thought about it. And if they haven’t thought about it, you shouldn’t be paying them.

You start hiring better. Once you’ve heard one professional walk you through a clean ROI projection, every other conversation gets compared to it. The bar goes up. The quality of your team goes up.

That single shift — from cost-thinking to ROI-thinking — is what separates the people who build effective Family Offices from the people who keep DIY-ing strategies they shouldn’t be doing themselves.

Key Takeaways

CPAs come in a spectrum — reactive at the bottom, proactive at the top. The proactive ones earn additional credentials (CTP, CTS) that signal they design strategy before the year ends. Most people pick a CPA without knowing this spectrum exists.

Reactive = “what you pay.” Proactive = “let’s plan to pay less.” That single shift is where the real ROI lives. A great CPA at the proactive end will quote you a savings number alongside their fee. A reactive one will only quote you the fee.

“What does it cost?” is the wrong question for any professional you hire. The right frame is ROI — what dollars will I get back relative to the dollars I’m paying? Strong professionals welcome that conversation. Weak ones dodge it.

Your Action This Week

Two questions worth sitting with:

First: Of all the financial professionals on your team — CPA, bookkeeper, attorney, advisor — do I actually know the dollar ROI of each relationship? If no, that’s a conversation worth having. The right professional will walk you through it gladly. The wrong one will say “it depends.” You’ll learn everything you need from that single response.

Second (the bigger one): Is my CPA at the reactive end of the spectrum or the proactive end? Ask them directly: “Do you hold the Certified Tax Planner or Certified Tax Strategist designation — and if not, can you walk me through the proactive plays you’d recommend for my situation this year?” The answer tells you everything. And if they’re at the reactive end, that’s not a failure — it just means there’s a proactive tier above your current setup, and that’s where the real savings live.

Let’s keep building.

—Christopher

P.S. The Two-Company Architecture I walked through last week is only as good as the team that operates it. The right CPA, the right bookkeeper, the right tax planner — those are the people who turn the structure into actual savings. If you haven’t yet seen how the whole Family Office system fits together — from the foundation up — The WealthOps Way is the on-ramp. It’s a free, 2-hour live workshop where I teach the foundational framework. No pitch. Just the structure, taught from the beginning.

Go Deeper

🎯 Start here if you’re new to this — The WealthOps Way Free, 2-hour live workshop. The foundation: what a Micro Family Office is, the two portfolio models, the 7 Components, and your own Legacy Statement.

Last week’s issue: Why I Built Two Companies for My Money — the entity architecture this newsletter’s professionals are needed to run.

This is education, not advice. Tax laws change frequently — verify current rules with qualified professionals. Learn the systems, don’t copy blindly.

Join me for The Micro Family Office Blueprint—our free live workshop designed to help you stop guessing and start running your wealth like a business.

You’ll go from scattered to strategic as you craft your own Portfolio Thesis—the foundation of everything that follows.

Spots are limited—and the clarity you’ll gain? Game-changing.

Let’s build your portfolio like it’s your next great company!

If you like the newsletter, support us by letting us know what you think (one click); please do that now!

PS...If you're enjoying Managing Tech Millions, please consider referring this edition to a friend.

If this was useful, tap the ❤️ button. It tells Substack to show more writing like this.

And whenever you are ready, there three ways I can help you:

Follow me on LinkedIn: Get more insights and real-time updates.

Watch on YouTube: Dive deeper into wealth strategies and interviews.

Get in Touch: Ready for a bigger move? Let’s talk.

Disclaimer: This newsletter is for informational purposes only and does not constitute financial or career advice. Always consult with qualified professionals before making any decisions based on the information provided.

Isn't the delta between 22k and 10k equal 12k not 14k?